05 Sep Invoices

Setting up your Invoices

The information in your invoices and even what you call them (‘tax invoice’ or ‘invoice’) depends on whether your business is registered for GST.

Whether you print your own invoices (for a paper-based system) or input details into an electronic system, you need to ensure your invoices contain all the information necessary to meet our requirements.

If you’re registered for GST, your invoices should be called ‘tax invoice’.

If you’re not registered for GST, your invoices should not include the words ‘tax invoice’ – you must issue normal invoices.

Below are examples of how tax invoices and invoices can look, including what information needs to be included on them.

Issuing Tax Invoices

When you make a taxable sale of more than $82.50 (including GST), your GST-registered customers need a tax invoice from you to be able to claim a credit for the GST in the purchase price.

If a customer asks you for a tax invoice, you must provide one within 28 days of their request.

Requirements of Tax Invoices

Tax invoices for taxable sales of less than $1,000 must include enough information to clearly determine the following seven details:

- that the document is intended to be a tax invoice

- the seller’s identity

- the seller’s Australian Business Number (ABN)

- the date the invoice was issued

- a brief description of the items sold, including the quantity (if applicable) and the price

- the GST amount (if any) payable – this can be shown separately or, if the GST amount is exactly one-eleventh of the total price, as a statement such as ‘Total price includes GST’

- the extent to which each sale on the invoice is a taxable sale (that is, the extent to which each sale includes GST)

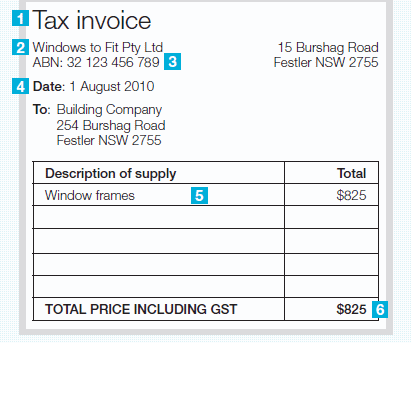

- Example 1, below, meets this requirement because the sale is clearly identified as being fully taxable by the words ‘total price including GST’

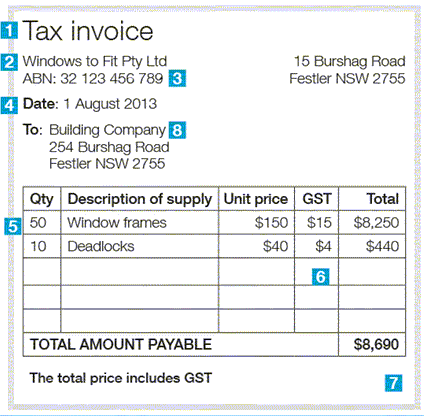

- Example 2 meets this requirement in two ways: it shows the GST included in each line item (see column with the GST amount), and the sale is clearly identified as being fully taxable by the words ‘the total price includes GST’.

In addition, tax invoices for sales of $1,000 or more need to show:

- the buyer’s identity or ABN

If your tax invoices meet the requirements for sales of $1,000 or more, you can also use them for sales of lesser amounts.

| Example 1: Tax invoice for a sale under $1,000 | Example 2: Tax invoice for a sale of more than $1,000 |

|---|---|

|

|

Taxable and Non-taxable Sales

A tax invoice that includes taxable and non-taxable items – that is, items that are either GST-free or input-taxed – must clearly show which items are taxable. In addition to the standard information the tax invoice must also show:

- each taxable sale

- the amount of GST to be paid

- the total amount to be paid.

Agency Relationships

Special rules apply to tax invoices for transactions carried out through agents.

Recipient-Created Tax Invoices

In most cases, tax invoices are issued by the supplier. However, in special cases, you, as the purchaser or recipient of the goods or services, may issue a tax invoice for your purchases. This is known as a recipient-created tax invoice (RCTI).

When you can issue an RCTI

You can issue an RCTI if:

- you and the supplier are both registered for GST

- you and the supplier agree in writing that you may issue an RCTI and they will not issue a tax invoice

- the agreement is current and effective when you issue the RCTI

- the goods or services being sold under the agreement are of the type the ATO have determined can be invoiced using an RCTI

Your written agreement can either be a separate document in which you specify the supplies, or you can embed this information or specific terms in the tax invoice itself.

When an RCTI is valid

To be valid, an RCTI must contain sufficient information to clearly determine the standard requirements (except that it needs to show the document is intended to be a recipient-created tax invoice, not a standard tax invoice). In addition it must detail the purchaser’s identity or ABN. It must also show that, if GST is payable, it is payable by the supplier.

As the recipient, you must:

- issue the original or a copy of your RCTI to the supplier within 28 days of one of the following dates

- the date of the sale

- the date the value of the sale is determined

- retain the original or a copy of the RCTI

- reasonably comply with your obligations under the tax laws.

You must not issue a document that would otherwise be a RCTI on or after you or the supplier have failed to comply with any of the requirements of RCTIs.